The Hurricane Clean-Up Clock: How Florida Storm Victims Can Lose a Case Without Losing the Facts

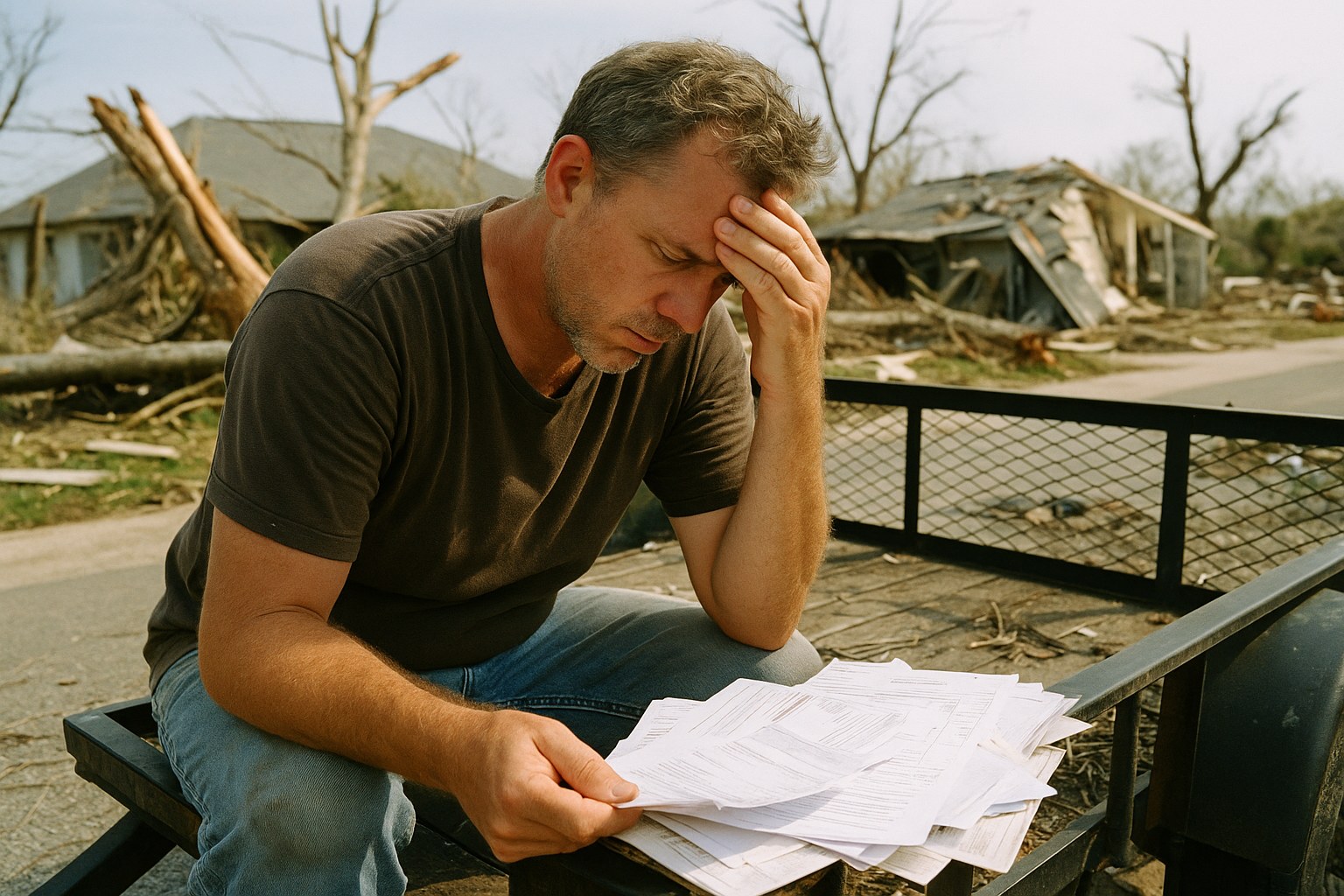

You filed a claim after the storm. You got a partial payment, a denial, or a long stretch of silence. You assume the real fight is still ahead: how bad the

7/14/2026 | 1 min read

Hurricane Claim Denied or Underpaid? Check Your Options

Hurricane claims require fast action. Take our 2-minute qualifier — free, no obligation.

See If You Qualify — Free Eligibility Check →No fees unless we win · Takes under 2 minutes · No obligation

The Hurricane Clean-Up Clock: How Florida Storm Victims Can Lose a Case Without Losing the Facts

You filed a claim after the storm. You got a partial payment, a denial, or a long stretch of silence. You assume the real fight is still ahead: how bad the damage really was, what it actually costs to fix, whether the adjuster lowballed you. For a lot of Florida homeowners and small business owners, that fight never happens. Not because the damage was not real, but because a deadline passed while everyone was still talking.

That is the part of storm litigation nobody warns you about at the kitchen table. A calendar can end a claim before a judge ever looks at your roof.

Why this matters to you in Florida

If someone owes you money or work after a hurricane, whether that is an insurance payout, a contractor's finished repair, or a vendor's promised delivery, time is not neutral. It is usually working against you.

Here is the uncomfortable dynamic. An insurer sends a partial denial. You disagree. You submit more photos, get a second estimate, go through an internal appeal, wait for a reinspection. Months pass. None of that is necessarily bad faith on their part. But the effect can be identical to stalling, because in many situations your own time limit to file suit keeps running the entire time you are being reasonable and patient.

The people on the other side have claims departments, defense counsel, and calendaring software whose entire job is tracking these dates. You have a tarp on your roof, a job, and a family. That gap is the whole problem.

What the law actually says

Florida law does push insurers to move. Under Fla. Stat. § 627.70131, insurers handling residential property claims are generally required to acknowledge a claim within a set number of days, begin investigating within a set number of days after a proof of loss, and pay or deny within a defined window, with limited exceptions that pause those counts. The Legislature has amended these claims-handling deadlines more than once in recent years, so check the current text at that link rather than relying on a number you heard secondhand.

But read that carefully, because it is the trap. Those deadlines govern how fast the insurer has to answer you. They say nothing about how long you have to sue once the insurer answers.

Your own clock is a separate thing:

Breach of a written contract. Florida's general civil limitations statute, Fla. Stat. § 95.11, sets the periods for civil actions, including actions founded on a written instrument. This is the framework that governs disputes with contractors, roofers, and vendors who took your money and did not finish the work.

Property insurance claims specifically. Florida has its own notice and suit deadlines for property insurance claims, and the Legislature shortened them significantly in recent sessions. These are in Florida's insurance code, not the general civil statute, and they are shorter than many people assume. Do not assume the general five-year figure you may have read applies to your hurricane claim.

Flood policies through the NFIP. This is the one that catches the most people. Claims tied to a flood policy issued under the National Flood Insurance Program are governed by federal law and the standard flood insurance policy, and legal commentary tracking NFIP litigation describes that window as roughly one year from the date of a written denial, with courts sometimes treating it strictly rather than pausing it during an ongoing appeal (Property Insurance Coverage Law Blog). That description comes from outside commentary, not from a statute or opinion analyzed here, so treat it as a reason to confirm your date quickly, not as a guaranteed rule in your case.

Notice the spread. Depending on which piece of paper your claim rests on, your window could be years or it could be roughly twelve months. Most people never learn which one applies to them until it is the wrong answer.

Why this pattern shows up after every hurricane

Courts do dismiss storm-damage cases on procedural grounds. Legal trade press has reported on breach-of-contract suits arising from Hurricane Helene damage being dismissed at the federal level (Mealey's, via Google News). That report does not state the grounds for the dismissal, and nothing here claims to know whether it was procedural, substantive, or something else. One case is not a trend, and it would be wrong to read it as one.

What can be said without guessing at any particular ruling is structural. In litigation tied to hurricanes, a filing deadline, a notice requirement, or a pleading defect can end a case before a court ever reaches whether the repairs were shoddy, whether the payment was owed, whether the damage was real. When that happens, the merits never get argued. The homeowner does not lose on the facts. The homeowner never gets to the facts.

And that dynamic quietly rewards delay. A vague denial letter, a claims process that meanders through an appeal, a contractor who stops returning calls: each one burns calendar. Deadlines exist in every area of contract law for good reasons, and that is not the complaint here. The complaint is the mismatch between who is equipped to track them and who is not.

What to do right now

This is general information about Florida law, not advice about your situation. That said, a few steps tend to protect a Florida policyholder's position regardless of how the case shakes out.

Write down every date that could start a clock. Date of loss. Date of any written denial or partial denial. Date of any written breach by a contractor or vendor. The date on a denial letter frequently controls when your time to sue begins, which is why the letter itself matters more than the phone call about it.

Find out which deadline governs your specific claim. A windstorm claim under a homeowners policy, a flood claim under an NFIP policy, and a contract claim against a roofer can carry three different windows on the same storm damage to the same house. Sorting out which applies is not something to do from a blog post, including this one.

Do not assume talking pauses anything. An open appeal, an active negotiation, or an adjuster saying "we are still reviewing it" often does not stop a limitations clock. Many Florida policyholders learn this at exactly the wrong moment.

Keep everything in writing. Save every letter, email, estimate, and photo, with dates. If a deadline dispute ever arises, that paper trail is the argument.

Ask early rather than late. Depending on the policy, the contract, and the facts, options that may be available under Florida law include a breach of contract claim, in some circumstances a statutory bad faith claim against an insurer, or preserving evidence for a later proceeding. Which of those is realistic depends entirely on your specific documents, and every one of them gets harder as the calendar moves.

This article is general information about Florida law and recent litigation trends. It is not legal advice, and it does not create an attorney-client relationship. Deadlines and rights vary by policy, contract, and circumstance, and this piece is not a substitute for individualized legal counsel.

If you are dealing with unresolved hurricane damage, a denied or delayed insurance claim, or a contractor who never finished the job, it is worth having a Florida attorney look at your deadlines before more time passes. Louis Law Group offers consultations for Florida residents and businesses who want to understand where they stand. The sooner you know which clock you are on, the more options you have.

Sources

- Fla. Stat. § 95.11, Limitations Other Than for the Recovery of Real Property

- Fla. Stat. § 627.70131, Insurer's Duty to Acknowledge and Act Promptly

- Federal Judge Dismisses Breach Of Contract Suit Arising From Hurricane Helene Damage, Mealey's

- National Flood Claims Have a One-Year Statute of Limitations, Property Insurance Coverage Law Blog

Is your insurance company handling your claim fairly?

Answer 5 questions. We'll analyze your claim against Florida property insurance law and show you exactly where you stand.

General information only, not legal advice. Based on Florida insurance law and claim best practices.

Get Your Free Property Damage Checklist

24-step claim guide — protect your rights after damage to your home

Free. No spam. Unsubscribe anytime.

Hurricane Claim? Find Out If You Qualify — Free Case Review

No fees unless we win · 100% confidential · Same-day response

★★★★★ 4.7 · 67 Google Reviews

What Our Clients Say

Real reviews from real clients who fought their insurance companies — and won.

"Citizens denied our roof leak claim, but this firm fought for us and got money for our repairs. We even had funds left over after fixing the roof."

"Pierre and his team are amazing. They truly cater to their clients and help you get the most from your insurance company."

"When my insurance company denied my roof damage claim, Louis Law Group stepped in and fought for me. I'm extremely satisfied with the results they obtained."

"They accomplished exactly what they set out to do and helped me finally receive my insurance check."

"Louis Law Group handled our homeowners insurance dispute and got results much faster than we expected. Excellent service and great communication."

"Very professional attorneys with outstanding attention to detail. They will not stop fighting for their clients."

* Reviews from Google. Results may vary by case.

How it Works

No Win, No Fee

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

You can expect transparent communication, prompt updates, and a commitment to achieving the best possible outcome for your case.

Free Case EvaluationLet's get in touch

We like to simplify our intake process. From submitting your claim to finalizing your case, our streamlined approach ensures a hassle-free experience. Our legal team is dedicated to making this process as efficient and straightforward as possible.

12 S.E. 7th Street, Suite 805, Fort Lauderdale, FL 33301